No Money Down vs Sign and Drive: What’s the Difference?

Picture this: You’re a proud, longtime, pre-owned car buyer. You love the idea of purchasing and owning a car, driving it into the ground without any restrictions and calling it your own. However, the allure of driving a brand new, state-of-the-art model straight off the lot has always been enticing, and it’s never been more tempting than it is now, with auto manufacturers rolling out deals left and right.

So, you do some research on cars you like, the must-have features you want to be included, and what you want your monthly budget to be around. You lock in on that luxury SUV you’ve had your eye on for a while, but always seemed unattainable. The excitement of driving off from the dealership in your new ride is firmly planted in your brain and you delve deeper into some of the offers that are out there on your soon-to-be dream car turned reality. That’s when you see the two phrases that seem to start off each ad…

“Lease for No Money Down” and “Sign and Drive Offer”

What’s the difference you ask? Which one is the better deal for me?

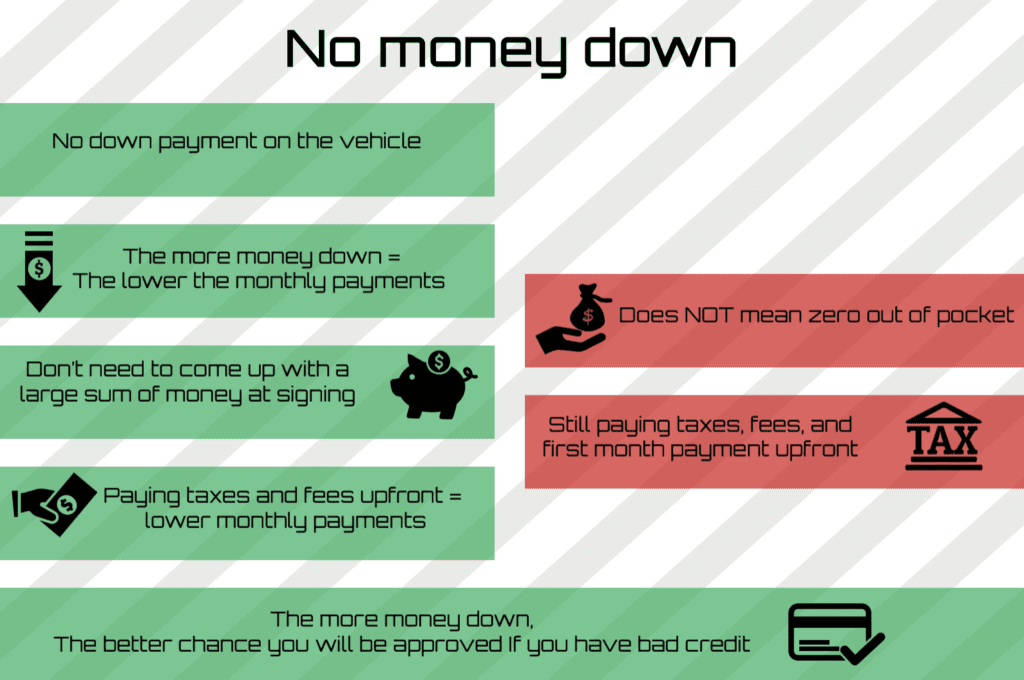

No Money Down

When leasing or financing a vehicle, your total lease cost is determined by a few factors: the total lease price of the car, your credit score, sales tax, assorted fees and how much you are willing to put toward the total purchase or lease price of the car, AKA, your down payment.

Put more money down at signing towards the car and you’ll see a lower monthly payment. Put no money down, and you’ll see your monthly payments increase or stay the same.

Typically, lessees don’t want to put a lot of money down toward their newly leased vehicle, since they will be returning it to the dealership in approximately two to three years. Due to this, many dealerships will advertise vehicle prices with just that – “zero money down.” This will keep the monthly cost of the vehicle a little higher, but consumers will have the peace of mind that they don’t need to shell out a lot of cash all at once.

Although it is much more common to see a down payment applied to a vehicle that is being financed as opposed to being leased, sometimes making a down payment on a lease is in the lessee’s best interest. If you do have extra cash to spare at the time of your new lease, making a sizeable down payment will take a chunk out of the total lease amount you are responsible for, thus knocking down your monthly payments. This option could be an attractive one for those looking to keep monthly costs down, while still driving a car that they desire.

Also, attaching a down payment to your lease could help you get approved in situations where your credit standing isn’t the best, but we’ll touch on that a bit later.

No Money Down Does NOT Mean Zero Out of Pocket

However, just because an ad says zero down, it doesn’t exactly mean your due at signing will be zero dollars.

The lessee will still be responsible for paying for other various fee associated with the lease, including the tax on the lease duration cost of the vehicle. This equals the vehicle sale price minus the residual value of the vehicle at the end of the lease.

In addition, there’s the first-month payment lease payment, as well as any fees (DMV, Bank, Dealership, etc) associated with the transaction, before acquiring the vehicle. This could potentially mean paying thousands of dollars at signing, depending on how expensive the vehicle is.

Some folks are okay paying these upfront costs when purchasing the car, some have a set amount of that total number they are willing to pay at signing and others don’t want to pay anything at signing, bringing us to our next (and most popular) option…..

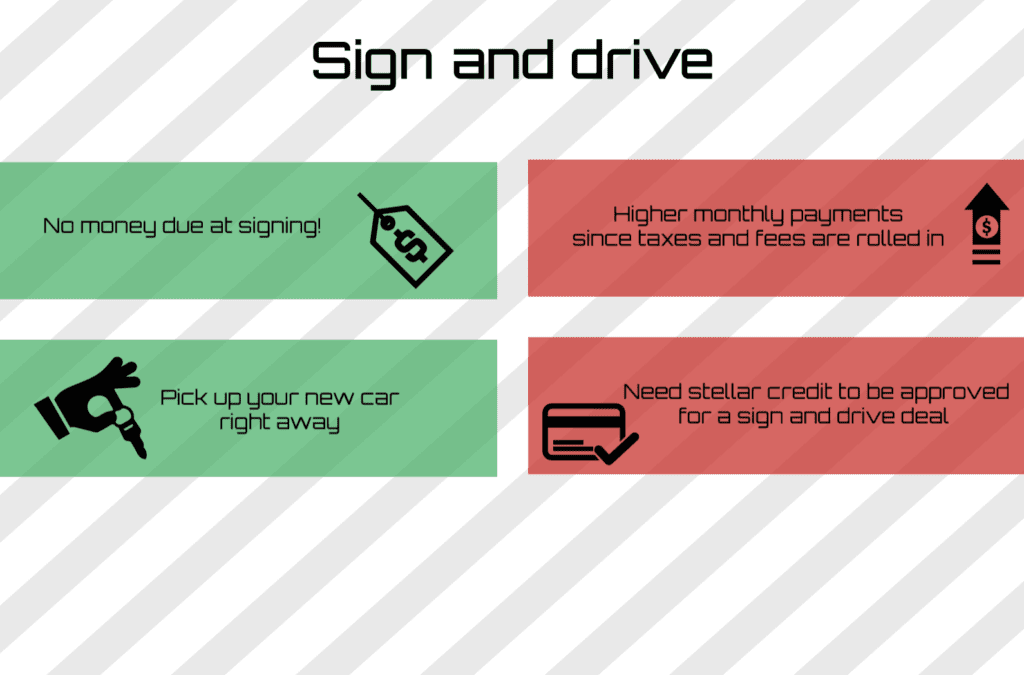

Sign and Drive Deals

A sign and drive deal is an extremely popular pay structure amongst lessees since it allows the consumer to drive off in a new car without paying anything at signing, which is why it’s literally called a “Sign and Drive deal.” Or, as Volkswagen pointed out a few years back, it’s actually more of a sign THEN drive deal.

A major benefit of this type of deal structure is that you don’t have a large upfront cost when picking up your new car from the dealership. This is seen as a favorable scenario for many reasons, but none moreover than simply because you can drive off in a brand new car without paying a cent.

However, that doesn’t mean that those due at signing costs just disappear. The costs are rolled into your monthly payments, divided by the total number of lease payments you owe, which can significantly raise the price of said monthly payments.

For example, if your monthly lease payment before upfront costs is at $321/month on a 36-month lease, and you owe $2,200 in taxes and fees that you want to be rolled into those payments, your new payment would be at a much higher price of $382/month.

That’s a $61 increase in your monthly payments which may push you out of the range of your desired monthly budget. It also has the potential to make relatively inexpensive monthly leases a tad more pricey, leaving you with a car you might not be able to afford on a month to month basis.

Which Type of Deal is Right for Me?

The type of lease deal that is right for you depends on a few factors. Your financial standing and credit history are the most important, as they will determine which deals you are even eligible for.

Individuals with poor to average credit will most of the time not even qualify for a sign and drive lease deal and dealerships may not offer as deep a discount on sign and drive offers. Only individuals with stellar credit history in most cases will even be eligible to move forward with a sign and drive deal, since, from the bank’s perspective, there is less risk associated with loaning them more money.

Therefore even if you decide that a sign and drive deal is the most attractive option for you and you have your heart set on signing one, you’ll still need to get approved by the lender in order to actually move forward with the deal.

However, if you are able to get approved for a sign & drive lease, this is a great option for potential lessees and one that many will ultimately end up choosing.

On the other hand, some consumers will find that structuring their lease with lower monthly payments is more favorable, since the payments will be more manageable over the duration of the lease – even with a larger sum paid at signing.

These deals will also be easier to get approved for since you are guaranteeing money upfront to the bank, meaning less cash they are on the hook for if you default on your payments. It could also allow you to drive a vehicle with more options and features, since you’ll be able to extend into a higher monthly budget with new, lower payments.

Lastly, if you have the extra cash to spare, you could opt to make a down payment on the lease cost of the vehicle, in order to knock your monthly payments down substantially. However, in the event that your vehicle is involved in an accident and is totaled, you won’t be able to recoup your down payment.

Making a substantial down payment could also improve your lease approval odds if you have less than stellar credit.

Conclusion

Overall the difference between a no money down lease deal and sign and drive lease deal comes down to the taxes and fees. Once you figure out if you want to pay those costs upfront or in monthly increments, that will in a sense decide which lease structure is right for you.

There are pros and cons with both options, but in the end, the decision will come down to personal preference, along with your financial and credit standing.

Here at Capital Motor Cars, we work with clients of all credit scenarios as well as financial situations, to structure lease payments that are the most comfortable for them.

Our team of experienced automotive coordinators will work to get you the best rates on the most aggressively priced cars in the region and deliver your new vehicle to your door. Contact us today to get started on your next (or first) lease!